VR Headset Sales Forecasts and Market Penetration 2014 – 2018

Building on our experience in producing market forecasts for the virtual world/MMO sector since 2006, in January 2014 we published the first ever market sizing forecast for the consumer virtual reality market. This forecast has now been updated and expanded to reflect the growing VR marketplace and the emergence of input devices to accompany HMDs. Our full (and free) updated VR market sizing report can be ordered here.

We’ll be diving into our findings in a series of articles, starting with addressable markets, HMD and input system penetration rates, available devices and overall unit sales forecasts for 2014 – 2018.

Addressable Markets and Penetration Rates

The starting point for our VR market sizing is the total global addressable market. We have defined the overall addressable market based on PC, Internet and Mobile Device availability, global gamers, socnet users and consumers residing in developed (as opposed to developing) countries.

On this basis we forecast the total universe for consumer VR at 800m consumers in 2014. Taking into account technology adoption rates and the fact that the VR market is in an emerging state, we have further refined the global universe from 800m down to 400m – this is the real addressable market.

From here we have segmented this total addressable market into three primary groups:

- Innovators / Hardcore Gamers: 2.5% of general popn. Eager to try new ideas and willing to take risks with new tech. Youngest age group of all adopters and highest social class. Innovators are the gate-keepers of promoting new ideas. Developer kit market, digital markers and VR enthusiasts.

- Early Adopters / Light Gamers: 13.5% of general popn. A closer social structure than Innovators, meaning they’re ‘Localites’. The highest ability to act as opinion formers across all other adoption types. Older tablet, mobile and console gamers.

- Early Majority / KT&T: 34% of general popn and an above average social class, adopting new ideas just before the avg. person. They interact frequently with their peers (locally and globally) as the important link in the diffusion process. Driven heavily by Kids, Tween and Teen market and active tablet, mobile and console gamers.

Further insight into these three markets is explained here. The chart below shows the addressable market for consumer VR by segment from 2014 to 2018.

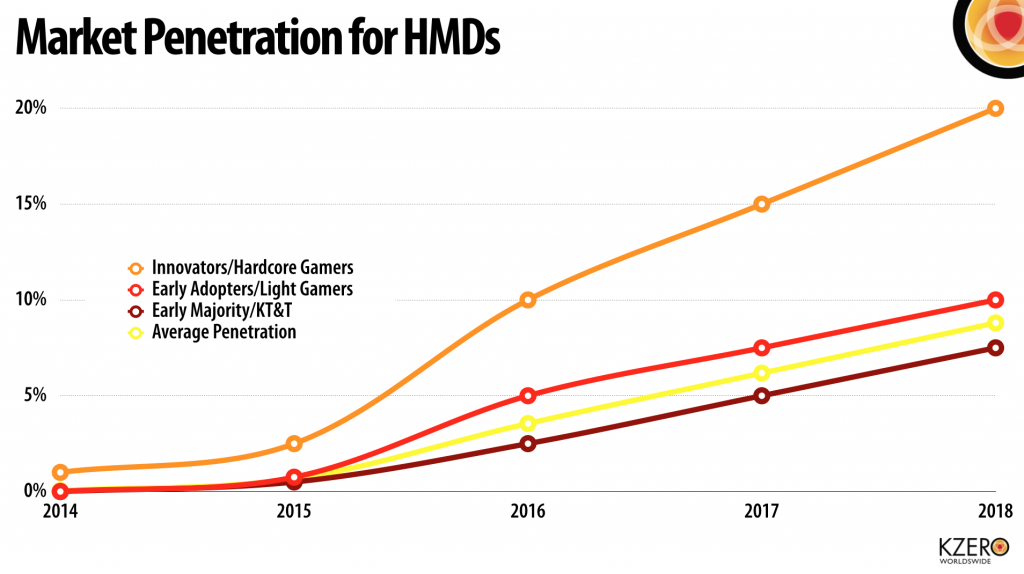

We have then applied forecasted penetration rates of consumers purchasing VR headsets (HMDs) by each of the three target markets. This is shown below:

The Innovator and Hardcore Gamer market is the segment we forecast to have the fastest and highest adoption rates for consumer VR headsets, representing 1% penetration in 2014 rising to 10% in 2016 and 20% by 2018. This market is at present being driven by Oculus DK1 owners, with DK2 purchases from Q3 2014 onwards (and in-part by Durovis Dive). From 2015 onwards we expect further penetration across all three groups as more HMDs come to market (this is explained below).

The Early Majority and Light Gamers segment is forecasted to have the second highest penetration rates, starting at 0.75% in 2015 rising to 10% by 2018. The third group, Early Majority and KT&T (Kids, Tweens and Teens) is predicted to reach 7.5% total addressable market penetration by 2018. On an overall basis, we forecast total penetration of consumer VR headsets to reach 8.8% by 2018.

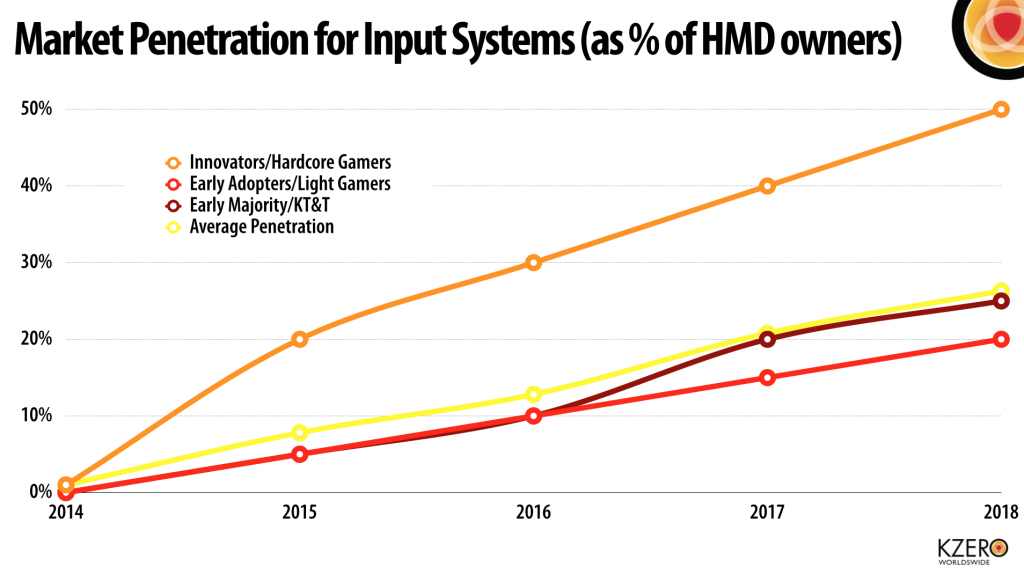

Looking at the market for peripheral hardware, i.e. input control systems for VR, this is a segment of the market we excluded from our January assessment. This is now included and our forecasted penetration rates (applied to the market of HMD owners) is shown below:

Particularly for gaming but additionally for other uses of VR such as Social Virtual Reality and UGC, we expect input systems to be very popular and we’re already tracking this market via our Hardware Radar. Penetration will start low in 2014 due to the low number of input devices we expect to be consumer-ready but will begin to ramp-up from 2015 with 20% of the Innovator market (that owns a HMD) to purchase a device and 5% respectively from the Early Adopter and Early Majority Groups. By 2018 we conservatively expect an average VR Input System penetration rate of 26%.

Devices for Sale

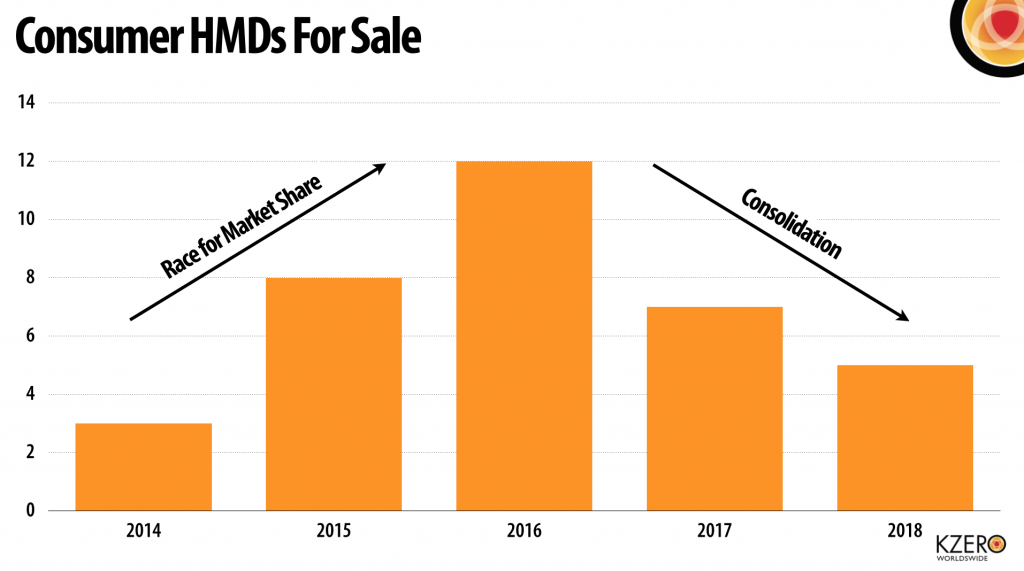

The chart below shows the predicted number of HMDs available for sale annually.

By the end of 2014 we envisage three products being available, namely the Oculus DK2, Durovis Dive and one other (possibly the Samsung Gear VR). A full list of companies developing VR headsets is here. The number of available headsets is then forecasted to ramp up quickly to eight in 2015 then 12 by 2015. However, we do not expect the market to support a large number of manufacturers and on this basis we believe there will be a period of consolidation from 2015 to 2018 as some companies struggle with market share and others are acquired.

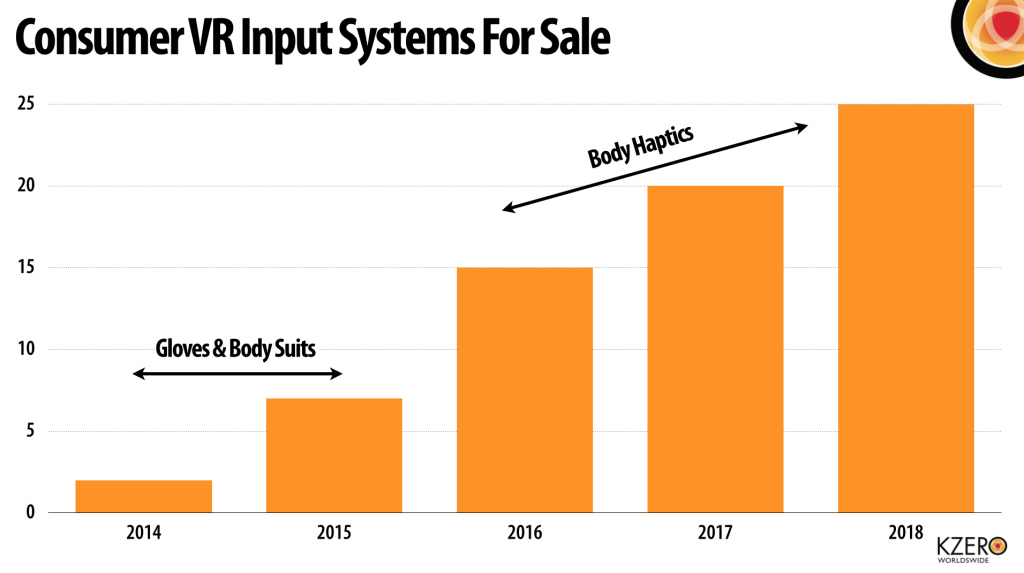

Although we expect consolidation in the HMD market we believe the inverse to be true in the input device category with a growing number of suppliers offering a wide range of peripheral equipment. This is shown below.

Products launched in 2015 are anticipated to focus on gloves and small body suits. From 2016 onwards we predict a growing number of haptic-led peripherals including chairs, full body suits and inevitably hardware catering to the sex market.

HMD Unit Sales

Applying forecasted penetration rates to the addressable markets produces unit sales, as shown below:

Total HMD unit sales in 2014 is forecasted at 200k, coming exclusively from the Innovator segment, driven primarily from the DK2. As the number of alternative suppliers begins to ramp up in 2015, total unit sales is forecasted at 2.7m, rising to 14.9m by 2016 as the market begins to open-up and attract Light Gamers (in the form of the Early Adopters) as well the KT&T market (within the early majority). By 2018 we estimate total HMD unit sales of almost 39m globally. This equates to a cumulative total of 83m HMD unit sales over the five year period.

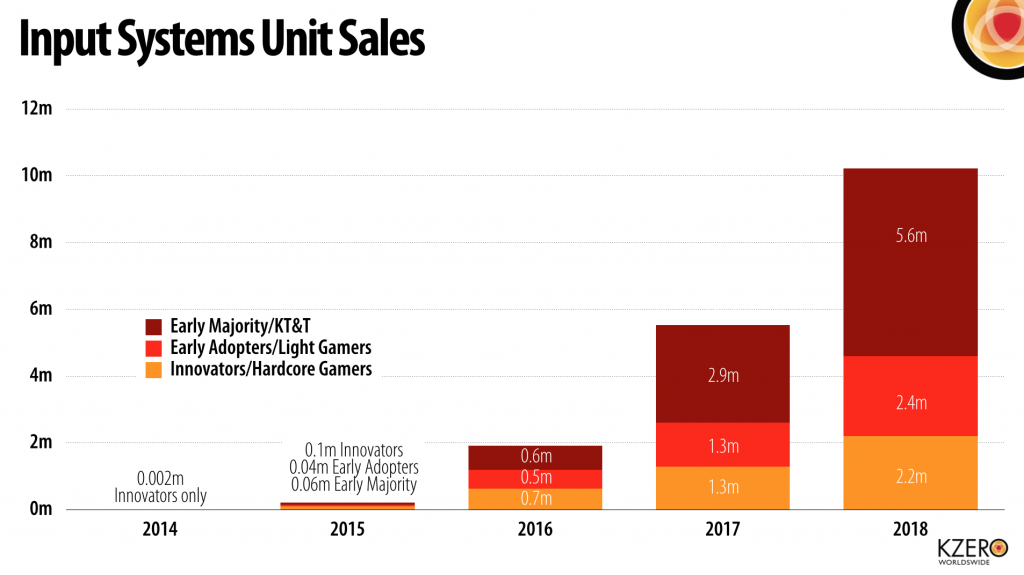

Input System Unit Sales

Obviously unit sales for input systems piggy-backs off the ownership base of HMDs. Our sales forecast is shown below. Sales are forecasted to reach almost 2m annually by 2016 relatively well spread across the three groups. In 2018 our forecast calculates circa 10m unit sales with the KT&T/Early Majority group accounting for just over 50% of total sales. Total cumulative unit sales of Input Systems over the period of 2014 to 2018 is forecasted at 17.8m

Related articles:

Further information:

4 Comments